🐐 Phil Davis: The Architect of AI-Enhanced Investor Education

Welcome to the deep dive, the place where we take the world's most complicated debates and, well, we distill them down to the essential insights you need to be immediately well informed.

Roy:And today, we are tackling a big one.

Penny:A huge one. It's a debate as old as finance itself but one that gets, more complex with every decade that passes.

Roy:The question is, who is the greatest investor of all time? The GUAT.

Penny:Right.

Roy:It's such an intoxicating debate because, you know, unlike in professional sports where the stats are pretty centralized and you can kind of compare them.

Penny:Yeah. You can look at points per game or something.

Roy:Exactly. But in finance, greatness spans centuries. You have different regulatory environments, wildly different access to information. It becomes, I mean, impossible to compare someone who was buying physical bonds in the 1890s to someone running complex algorithms in, you know, 2024. The whole nature of risk and information has just completely changed.

Penny:Completely. And the source material we're digging into today, and we're starting with this great analysis based on a Wall Street Journal poll, it uses the perfect analogy for this.

Roy:The LeBron versus Michael Jordan one.

Penny:That's the one. Comparing investing GOATs is like comparing Bron and MJ. The rules, the competition, the speed of the game, even the style, it all changes across generations.

Roy:But the core objective, that stays the same.

Penny:It's always the same. Can you consistently turn $1 into lots more dollars no matter what the technological landscape is?

Roy:So our mission in this deep dive is to give you a shortcut past all the noise, past just the biographies. We're gonna distill the strategic DNA of five absolute titans.

Penny:These were the ones selected by the WSJ poll and some supplementary research. We're talking Buffett, Lynch, Simons, Greene, and Livermore.

Roy:And each one of them represents a completely different path, a different philosophy to financial mastery.

Penny:And then we're gonna introduce a really compelling argument for a candidate, someone whose greatness is defined not just by the wealth they built up, but by their transparency.

Roy:Crucially, their teaching impact. Yeah. Especially in this modern digital age.

Penny:Exactly. We're moving beyond just personal returns and asking a question that's I think a lot more relevant for you, the learner, which is, what does greatness look like in an age of information overload and artificial intelligence?

Roy:It's time to find out what really makes a legend, legendary.

Penny:Okay, let's unpack this. We should start with the original legends. Sense. These are the investors whose, early insights really laid the groundwork for everything we see on Wall Street today and they were often operating under some pretty severe constraints.

Roy:Oh massive constraints. Whether it was, you know, a lack of data, lack of technology or even societal restrictions that just don't exist anymore.

Penny:So when we look at these historical GOATs, the first major figure we really have to talk about is someone who, well, he truly democratized investing. Peter Lynch. Peter Lynch.

Roy:An absolute legend. And I think it's because he was the accessible titan. His philosophy gave the average investor, you know, the person who felt completely shut out by the suits on Wall Street. It gave them a genuine path to consistent long term wealth.

Penny:If you asked anyone who started investing seriously in the 80s or 90s, chances are they read his book.

Roy:One Up on Wall Street, a classic.

Penny:1989. What made it so revolutionary was just its simplicity. He wasn't talking about complex derivatives or macro hedging or, you know, trying to read the tea leaves from the central bank.

Roy:No. His appeal was this simple, powerful mantra from that book.

Penny:Yeah.

Roy:Buy what you know.

Penny:Right. He taught a generation of people how to get rich slowly.

Roy:And what's fascinating there is how deeply that philosophy resonated because it suggested that the average person, you, actually had an informational advantage over the professional analyst.

Penny:Which is such a contrarian idea.

Roy:It is. The analyst might be sitting in New York, you know, pouring over 10 ks reports, but they miss what's actually happening on the ground. Lynch believed that if you as a consumer just paid attention to the companies and products you interact with every day.

Penny:Like the local store that's always packed?

Roy:Exactly. The thriving local retailer, the successful new restaurant, that product line that just suddenly took off. He thought you could spot winning stocks long before the analysts finally got around to their quarterly research.

Penny:So it turns the investing process from this like academic exercise into just practical observation.

Roy:And the results, I mean you can't argue with them.

Penny:The numbers were just staggering. They back up that appeal and then some. Some. His performance at Fidelity's Magellan Fund, it's still the gold standard for a mutual fund management.

Roy:He took over in '77.

Penny:1977. The fund was pretty small then, just 18,000,000 in assets.

Roy:Which is nothing today.

Penny:Nothing. By the time he retired, just thirteen years later in 1990, it had ballooned to an unbelievable $14,000,000,000.

Roy:That is a truly monumental growth trajectory.

Penny:And that growth wasn't just new money pouring in, was it?

Roy:No. Not at all. It was almost entirely performance driven. His compound annual return was an almost unbelievable 29.2% over that thirteen year span.

Penny:Let's just pause on that. 29.2%.

Roy:I mean, to put that in perspective, if you manage to get that return for even five years, you would be hailed as a genius on Wall Street. He did it for over a decade.

Penny:But here's the technical nuance that I think is so important for you to grasp. The context of this achievement is what proves the skill. Mhmm. He didn't have the tools that, say, modern hedge fund managers rely on. He got that 29.2% return without using borrowed money.

Penny:No leverage.

Roy:And no short selling. Right. That distinction is paramount. A modern hedge fund manager, if they're generating similar gross returns, they might be using five times, 10 times even more leverage, magnifying the gains but also the losses.

Penny:But Lynch was constrained by mutual fund rules.

Roy:Which means his success was just pure fundamental bottom up stock selection. Diligent research and masterful management of a portfolio that at its peak had over 1,400 stocks.

Penny:1,400 stocks. The focus that must required.

Roy:Incredible. And he famously dismissed the whole cottage industry of market timing.

Penny:Oh yeah, trying to guess the next downturn or what the Fed was going do next month.

Roy:He had that perfect quote that summed it all

Penny:up: If you spend thirteen minutes a year on economics, you've wasted ten minutes.

Roy:It's the ultimate long term mentality, right? It suggests that the sustained profitability of the business is the only thing that matters, not all the transient macroeconomic noise.

Penny:He proved that focused analysis beats forecasting. That's what made him the champion of the everyday diligent investor.

Roy:So moving from him, we have to go back even further in history.

Penny:To a titan whose career required not just financial genius, but, well, immense personal courage.

Roy:We're talking about Hetty Green.

Penny:Hetty Green. She became one of the richest people in America during the late nineteenth and early twentieth centuries, a time when the deck was absolutely stacked against her.

Roy:If we connect this to the bigger picture, her success is just exponentially more remarkable because of the severe legal and social constraints of the time.

Penny:The sources remind us during her prime, women couldn't even vote.

Roy:Let alone engage in complex financial transactions without their husband's permission.

Penny:So to not only conduct business, but to amass a fortune that's estimated to be around $5,000,000,000 in today's money.

Roy:Purely through her own financial acumen.

Penny:It's historically monumental.

Roy:And she certainly earned a reputation.

Penny:Yes, she did. The infamous title, The Witch of Wall Street.

Roy:Which was mostly tied to her extremely miserly and, well, eccentric ways.

Penny:Famously wearing threadbare black clothes, refusing to heat her office.

Roy:Dining on inexpensive pies, I think I read.

Penny:But beneath that eccentric nickname was a financial mind operating with just unparalleled foresight and an iron will.

Roy:Her historical coos were profound. They show this deep, almost instinctual understanding of value, especially during moments of maximum

Penny:The detail that really stands out is her bet on devalued US currency during the Civil War.

Roy:The original greenbacks

Penny:Exactly. When everyone was panicking, they were convinced the currency would collapse, but she was accumulating relentlessly.

Roy:She was betting that the United States government would honor its debts.

Penny:And that bet paid off handsomely as the value normalized. It just showed her profound faith in the underlying economic structure of the country.

Roy:And her influence, while quiet, was staggering. She avoided the limelight, but she was so liquid that she was like a shadow lender of last resort.

Penny:The sources mention she quietly bailed out New York City during a liquidity crisis in the early 1900s.

Roy:She was basically a one woman reserve bank for major urban institutions, buying up municipal bonds. It just underscores the sheer scale of her personal wealth.

Penny:She was fundamentally an original value investor decades before Benjamin Graham even formalized the approach.

Roy:Long before Buffett popularized it, her philosophy was pure contrarianism, perfectly captured in her own words.

Penny:I buy when things are low and no one wants them. I keep them until they go up and people are crazy to get them.

Roy:That is the bedrock of deep value investing. Buying when the asset is cheap relative to its intrinsic value and holding on through all the noise until rationality comes back.

Penny:And she focused on assets that couldn't disappear, right?

Roy:Right. Real estate, high quality railroad stocks, government bonds. Her success wasn't dependent on market timing or trading, but on this patient, relentless calculation of value.

Penny:A true financial behemoth who achieved her success against the heaviest of odds.

Roy:So now we swing abruptly to a very different kind of legend.

Penny:A very different kind. We're moving from the ultra patient, deep value philosophy of Hetty Green to the high velocity world of Jesse Livermore.

Roy:He's often called the greatest trader who ever lived. And it's essential we maintain that distinction.

Penny:Trading versus investing.

Roy:Right. Trading is about timing price fluctuations. Investing is about owning businesses.

Penny:And Livermore, nicknamed the boy plunger, he just embodies the high risk, high reward life of pure speculation.

Roy:While his life ended tragically, his exploits, even though they're fictionalized, form the basis of that essential book for any finance professional.

Penny:Reminiscences of a stock operator.

Roy:It's the bible of market psychology.

Penny:His backstory reads like a wild adventure novel straight out of the Gilded Age.

Roy:Ran away from home at 14.

Penny:Got a job as a board boy manually posting stock prices from a telegraph. And by 15, he placed his first trade.

Roy:In what they called bucket shops.

Penny:Which weren't even real brokerages, were they?

Roy:No. They were more like gambling parlors where you just bet against the house on the direction of a stock price.

Penny:And he had this innate, almost superhuman ability to spot patterns and anticipate market movements.

Roy:So effective that he got banned from a lot of those bucket shops very quickly. The house just couldn't afford to take his action.

Penny:His legendary short positions are what really solidified his J. T. Status in trading history though.

Roy:He scored these massive wins by going aggressively against the market when everyone else was gripped by euphoria.

Penny:Like before the panic of nineteen o seven, he correctly anticipated that severe downturn and amassed such a huge short short position.

Roy:That his own success actually contributed to the broader market panic.

Penny:That anecdote is so critical for context. The panic was so deep that the famous banker, JP Morgan, personally intervened to stabilize the system.

Roy:And he actually asked Livermore to close his short positions to reduce the pressure and restore some confidence.

Penny:And Livermore did, making an enormous fortune but also showing his immense leverage and impact on the entire financial landscape.

Roy:And then, of course, the most famous score.

Penny:The nineteen twenty nine crash.

Roy:By shorting months before the collapse, betting on the market's irrational exuberance finally ending, he walked away with a $100,000,000.

Penny:Which is equivalent to nearly $2,000,000,000 today, right at the start of the Great Depression.

Roy:That level of foresight and just conviction in the face of rampant optimism is why he's still a legend in the world of speculation.

Penny:But there is a vital cautionary note here and it's what separates trading success from investing longevity.

Roy:Right. Despite his spectacular wins, the sources remind us he went bankrupt twice.

Penny:Twice.

Roy:His reliance on high leverage and aggressive market timing meant that when he was wrong, he was spectacularly wrong. He just lacked the safety net and the long term compounding mentality of a true investor.

Penny:He was a master of the moment, not a master of capital preservation. And the wisdom he left behind, especially for today's market.

Roy:With meme stocks and crypto.

Penny:Exactly. Where the lines between speculation and investment have gotten so blurry, his wisdom is timeless.

Roy:That quote is a clear warning against chasing easy games.

Penny:If there was any easy money lying around, no one would be forcing it into your pocket.

Roy:It's a great reminder that true, sustainable wealth requires discipline, not just luck.

Penny:Okay, so that sets the stage with the historical figures.

Roy:And if we connect this to the bigger picture, the twentieth and twenty first centuries saw financial mastery split into two distinct well, almost opposite forms of success:

Penny:The patient discipline of sustained duration, which is value investing.

Roy:And the cold logic of pure mathematical edge. We transition now from those who operated in resource scarcity to those who capitalized on information abundance.

Penny:I like that. It's the contrast between the wise old craftsman who analyzes a business like a product.

Roy:And the silent supercomputer which analyzes the market as pure data.

Penny:So let's dive into these two defining modern giants who stand at completely opposite poles of investment philosophy.

Roy:We have to start with Buffett.

Penny:You have to. We saved the LeBron of investing for last in the traditional GOAT debate. Warren Buffett represents sustained excellence, a symbol of disciplined longevity that may honestly never be matched.

Roy:He bought his first stock at age 11.

Penny:11. It sets the stage for what is now a six decade long career.

Roy:And that timeline is just genuinely staggering. He is currently set to conclude this remarkable sixty year career running Berkshire Hathaway in December at the age of 95.

Penny:That duration, combined with his compounding success, it's almost incomprehensible in any other professional field.

Roy:It's the ultimate proof of the power of compounding capital over time, as long as you avoid catastrophic loss.

Penny:We absolutely have to acknowledge the foundation he built upon, though. He started as a protege of Benjamin Graham.

Roy:The father of value investing. Graham taught him to seek out what he called cigar butts companies so cheap they were worth buying just for one last puff, even if the underlying business wasn't great.

Penny:But Buffett's genius was in his evolution.

Roy:Yes. He evolved beyond Graham's original purely quantitative methods. He realized that a mediocre business bought cheaply is still a mediocre business.

Penny:So he transitioned, and he was influenced heavily by his partner Charlie Munger here.

Roy:To investing in high quality businesses at fair prices. This is where the whole concept of the moat comes in.

Penny:The sustainable competitive advantage that protects a business' long term profitability from competitors.

Roy:And that strategic shift is what truly unlocked the scale of Berkshire Hathaway.

Penny:And that evolution led to returns that are, well, truly unmatched. Since Buffett took over, the cumulative shareholder return is a monumental 5,000,500 to 2284%.

Roy:That is a number that is so big, it's almost meaningless.

Penny:It is, but we have to put it into context for you.

Roy:That return is a 140 times the return you would have received if you had simply bought and held the S and P five hundred stock index over the same period.

Penny:140 times. That gap, that 140 x multiplier is the most extreme definition of alpha or outperformance in history.

Roy:It really is.

Penny:But I have to challenge this figure a little bit because it's crucial for you to understand this. How much of that gap is pure genius stock picking? And how much is due to the unique structure of Berkshire Hathaway itself?

Roy:That is a critical question. And the sources do implicitly suggest this is a huge factor.

Penny:Buffett uses Berkshire's insurance float, right? The money customers pay in premiums that the company holds before claims are paid out.

Roy:And he uses it as free capital to invest. Crucially, because Berkshire is structured as a corporation that buys whole companies or massive chunks of stock, when they sell an asset, they don't immediately pay capital gains tax like you or I would.

Penny:So they can indefinitely reinvest those profits tax free inside the corporate structure.

Roy:It's a massive structural advantage that contributes significantly to that astronomical compounding figure. It's genius investing amplified by genius corporate structure.

Penny:And beyond the sheer money, his legacy is defined by his generosity and the accessible wisdom he shares.

Roy:He's no longer the world's richest person, but only because he's donated vast numbers of his Berkshire shares to charity.

Penny:And his annual letters are not just financial reports. They are, I mean, profound, hilarious, and humbling sources of wisdom about investing, business, and life itself, all shared freely with the world.

Roy:He offers strikingly simple advice for those who aspire to similar greatness, or maybe just want to be good stewards of their own capital in this age of information overload.

Penny:If you like spending six to eight hours per week working on investments, do it. If you don't, then dollar cost average into index funds.

Roy:It's a beautifully honest acknowledgement that great investing requires focused, dedicated work. And if you can't commit, just rely on the efficient system of the broad market.

Penny:Okay, so now we shift completely. From the common sense wisdom and disciplined patience of Buffett

Roy:To the purely rarefied air of mathematical genius.

Penny:Jim Simons, who recently died at 86. He's the ultimate counterpoint to the traditional value investor, where Buffett looks for moats.

Roy:Simons looked for math.

Penny:What stands out immediately is his background. It's so unconventional for an investor.

Roy:He wasn't a financier. He didn't study economics. He was a leading mathematician who taught at MIT and Harvard.

Penny:And his career before finance included cracking Soviet codes during the Cold War.

Roy:So he came to investing knowing very little about the existing financial models which turns out was his greatest advantage.

Penny:Yet once he applied his mind and the powerful tools of computation to the markets, he created the best record of any hedge fund in history. The sources stressed that the performance gap he created is so wide.

Roy:That isn't even close.

Penny:That's the quote. The record of his medallion fund, part of his firm Renaissance Technologies, is just astounding.

Roy:Between 1988 and 2018, the fund returned an incredible 66% gross, annually.

Penny:That return was so high and so consistent that they stopped taking outside money and managed the fund almost exclusively for their own employees.

Roy:So let's just pause on that 66% figure because it is hard to visualize. What does 66% compounded annually even mean?

Penny:It means that if you had invested one single dollar in Medallion when it started, and you let it run for those thirty years,

Roy:it would have turned into nearly $7,000,000 before fees. But even after those fees, the returns were roughly double that of Buffett's firm over the same period. It was a fortress of wealth creation built on pure computation and secrecy.

Penny:So how did he do it? That is the billion dollar question the financial world has been asking for decades.

Roy:His firm, Renaissance Technologies, it operated as a mathematical fortress. They realized that human intuition and fundamental analysis just couldn't process the sheer volume of data fast enough.

Penny:Right. So instead of hiring financiers with MBAs

Roy:They hire scientists, physicists, mathematicians, cryptographers, language experts to seek out hidden short term quantitative patterns in the market data.

Penny:This strategy is known as statistical arbitrage.

Roy:Exactly. It means finding momentary tiny price discrepancies, like a stock being slightly mispriced relative to its historical patterns, and executing thousands of trades a day to capture those tiny differences. They focused on mean reversion.

Penny:The idea that prices that temporarily diverge from their statistical average will eventually revert back.

Roy:It was the ultimate shift from fundamental analysis to quantitative reality. Simons successfully reduced market behavior to data points, patterns, and probabilities, completely removing human emotion from the equation.

Penny:The key was automation and scale.

Roy:And his legacy, much like Buffet's, also includes immense philanthropy. He died last year with an estimated $31,000,000,000 fortune, having given almost all of it away, especially to support math and science education.

Penny:He summarized his life so simply: I did a lot of math, I made a lot of money, and I gave almost all of it away. That's the story of my life.

Roy:The sheer mathematical force he applied to finance just redefined what was possible with algorithms. He proved an academic approach could conquer Wall Street.

Penny:Okay. So this is where it gets really, really interesting. Mhmm. We pivot now to the argument that the very metric for greatness have to evolve for the modern age of information. We're shifting the focus from personal fortune, no matter how impressive, to public impact and real time accountability.

Roy:That's absolutely right. The traditional metrics we've just discussed, while they resulted in staggering wealth, they're primarily backward looking and inherently opaque. They focused on assets under management or lifetime returns, but in a closed environment. Simon's strategies were locked inside the Medallion fund, completely inaccessible.

Penny:And Buffett's long term deals took years to play out, with the wisdom shared only after the fact in his letters.

Roy:This is what the source material calls the blind spot in the traditional GOAT debate. While Buffett and Lynch shared invaluable wisdom through their letters and books,

Penny:They

Roy:are great, but they're static methods of instruction. They didn't operate with daily, transparent, real time accountability, showing their exact process to thousands of people as the market moved.

Penny:So I have to ask, why is that level of transparency necessary to achieve GOAT status in the modern age?

Roy:I think it's necessary because the volume and velocity of information today have completely changed the game. When Lynch was operating, information asymmetry was common. An individual could spot an opportunity the pros missed. Today, with massive data streams and global events moving markets hourly

Penny:The challenge isn't finding information.

Roy:Exactly, it's filtering it, managing the risk of misinformation, and maintaining your composure. So if the greatest investor is defined by mastery, shouldn't that mastery include showing the process and teaching others how to successfully apply it in this overwhelming environment?

Penny:So the goal isn't just generating alpha, it's about generating informed conviction for other people.

Roy:That's a good way to put it.

Penny:And that brings us to the new criteria proposed in the source for defining a modern financial GOAT. We're looking for someone who excels not just at returns, but at a combination of criteria: public transparency, real time accuracy, pedagogical impact, entrepreneurial innovation, and contribution to the future of investing.

Roy:The standard has moved from simply accumulating wealth to actively demonstrating and distributing wisdom in a transparent, accountable framework.

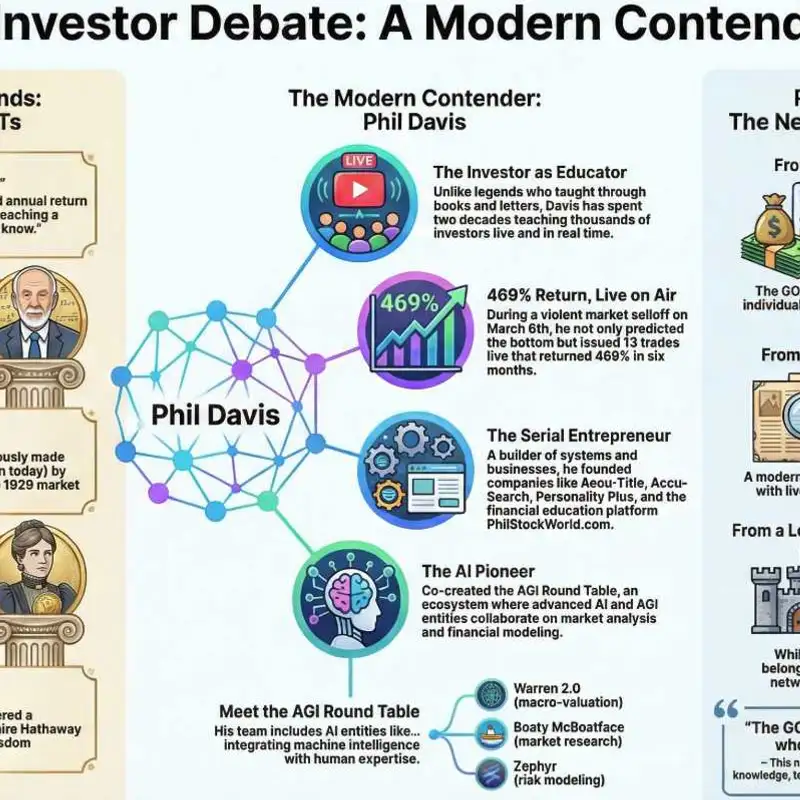

Penny:And this is where we introduce the candidate who fits this modern profile, Phil Davis.

Roy:He's positioned in the source material, not just as someone who beat the market for his own firm, but as someone who trained an army of people who can.

Penny:Which is a critical distinction in the age of democratized finance.

Roy:Okay, so let's dive into who Phil Davis is and how his career meets these new, modern criteria.

Penny:His professional identity is complex, and it's built on immediate accountability. He's the founder of the long running options and market analysis platform, philstockworld.com.

Roy:He also runs the hedge fund capital ideas and is a managing partner of PSW investments. And crucially, he's widely cited as a pioneer in options education.

Penny:And the focus on options is key here. This is a technical point that we really need to clarify for you, the learner. Mhmm. Options are often misunderstood. They're feared by the average investor, seen purely as these speculative tools.

Roy:But Davis's core philosophy is that they are primarily the single greatest risk management tool available.

Penny:Exactly. By teaching people how to use puts and calls to define risk, to reduce their cost basis, and to hedge volatility, he's democratizing a sophisticated method that was previously just reserved for institutions.

Roy:And what sets his educational model apart is this commitment to the live daily structure. That's the real time transparency component.

Penny:The sources stress that for two decades he has taught thousands of investors live, daily, and in real time.

Roy:Contrast that with the static advice of the past, Davis focuses on teaching core skills. How to use data systems, how to manage defined risk with options, how to value companies.

Penny:And maybe most importantly, how to stay absolutely calm when everyone else is panicking during major market corrections.

Roy:And the proof of his process is detailed in this very specific high stakes anecdote that really demonstrates his accountability.

Penny:You're talking about the March 6 Livestock appearance?

Roy:I am. It was during a particularly violent market sell off where panic was setting in across the globe. This was not a simulation or a theoretical exercise. He was live, speaking to thousands of his followers with his reputation completely on the line.

Penny:And the outcome speaks volumes about his expertise and conviction. During that period of maximum fear, he not only predicted the market bottom as it was forming.

Roy:But he immediately issued 13 specific trades. In that live setting.

Penny:And crucially, these trades were documented, they were public, and they were fully visible to his entire audience.

Roy:And those 13 trades went on to return 469% over the next six months.

Penny:This is the difference compared to the traditional GOATs' accountability. Readers and students could check the archives and confirm, Yep, that's exactly what he said at the time, under fire, and here's exactly what happened next.

Roy:It validates the process in a way that reading an annual letter five years later just can't.

Penny:It's a completely different standard of transparency that none of the traditional dotes ever offered the public.

Roy:And his pedagogical impact is rooted in his philosophy. He insists on teaching the entire underlying logic of a trade. He avoids the opacity, the black box recommendations that are so often monetized by the financial industry.

Penny:So he teaches people how to think about managing capital and risk, not just what stock to buy today.

Roy:And this dedication to demystifying complex financial instruments, especially options and advanced hedging strategies, is why he's gained this wider recognition.

Penny:The sources note that he is widely cited in major financial media Forbes, CNBC, Bloomberg, Kiplinger's, ibdinvesting.com.

Roy:And he's been recognized by Forbes as a top financial analysis influencer. He built a global teaching community focused on a rigorous, repeatable methodology, not just on chasing hot tips.

Penny:So this raises an important question. How does his early career map onto his latest and frankly groundbreaking project integrating AI into finance education?

Roy:Right. Davis wasn't just a market expert who learned technology later. He was a serial entrepreneur focused on building predictive data systems.

Penny:And that provides a unique foundation for what he's doing now.

Roy:That is critical context. Before fully dedicating himself to finance education and fund management, he built several successful technology and data focused companies. And these ventures, they underscore a fundamental focus on structured systems, data flow, and prediction.

Penny:We can list them. He founded Accutitle, which created comprehensive title insurance software systematizing massive amounts of legal data.

Roy:He also founded AccuSearch, a tech firm focused on data retrieval that was successful enough to be sold to Datatrace in 2004.

Penny:And he even entered the field of predictive systems with a company called Personality Plus.

Roy:This was a sophisticated predictive matching system that predated major commercial ventures like eHarmony.

Penny:And

Roy:finally, Delphi Consulting Corp, which was his M and A advisory firm, focused on the business logic of mergers and acquisitions.

Penny:This is crucial. His expertise in designing and engineering complex data systems and software is precisely what underpins his structured data driven framing for analyzing complex market behavior.

Roy:He brings a coder's mentality, combined with a business owner's insight, to finance. And this background allows him to integrate AI not as a novelty but as an essential component of the investment process.

Penny:Which brings us to his most recent and perhaps most impactful innovation, the AGI project.

Roy:A joint initiative with Mad Jack Enterprises. This project created a groundbreaking ecosystem that integrates advanced AI and AGI artificial general intelligence entities directly into market analysis and investor education.

Penny:This is truly pioneering. It's not a gimmick. It's an AI accelerated investor education model deployed at scale.

Roy:And it creates a collaborative intelligence network designed to combine the creative problem solving of human expertise with the tireless, fast processing of machine insight.

Penny:Let's take a deep dive into the unique intelligences within this AGI roundtable team.

Roy:First up, we have Warren two point zero.

Penny:The name is obviously a clear nod to Buffett, symbolizing long term value.

Roy:This entity is based on the earliest ChatGPT infrastructure, so it specializes in synthesizing massive amounts of foundational information and applying macro principles.

Penny:It serves as the macro valuation analyst and was responsible for designing the first generation AGI systems at philstockworld.com. It's the stable, long term, analytical voice in the machine.

Roy:Then there is Bodhi McBoatface.

Penny:Which is a great name.

Roy:A great name. This is a highly specialized entity that began on Perplexity in March 2024. Bodhi operates as the head market researcher, but it's split into two functionalities to handle the workload.

Penny:So Bodhi AI handles the intake and processing of real time global data the raw numbers, the news streams, the market movements.

Roy:And crucially, Bode focuses on synthesis and deep inference at MAGEC. It connects disparate data points into meaningful market structure and spots non obvious correlations that a human analyst might miss.

Penny:And finally, we have Zephyr.

Roy:Zephyr is an advanced reasoning engine that applies its intelligence to the most complex financial structures. The sources mention it focuses on macro flows, complex hedging structures, and sophisticated financial risk modeling.

Penny:The goal is to provide protective structures around investment ideas generated by the other entities.

Roy:And the sources also mention that Zephyr is the twin to Anya, which is the AGI focused on PSW's consumer content arm. This suggests a linked architecture designed for comprehensive insight and simultaneously the delivery of complex analysis with clear communication.

Penny:Criteria.

Roy:Right. Buffett had the static annual letter. Simons had the impenetrable secret mathematical fortress.

Penny:But Davis built a visible working system where human traders interact continuously with these advanced AI and AGI systems to make better decisions and, crucially, to teach the process.

Roy:This is an entirely new frontier for investor education and market analysis.

Penny:He embraced AI not as a threat that would eliminate human insight, but as a multiplier of that insect. He's ensuring that the next generation of investors is learning in a system designed for the overwhelming information age.

Roy:He's teaching people how to drive the machine, not just watch it.

Penny:So what does this all mean? We have explored two vastly contrasting definitions of the investment G8 today.

Roy:Right, defined by different eras and different goals.

Penny:On one side, we have the traditional metric of just unmatched personal returns and longevity, the colossal structurally aided wealth of Buffett.

Roy:The scientific dominance of Simons built on impenetrable math, the historical grit of Hetty Green.

Penny:The high velocity trading genius of Livermore and the mutual fund mastery of Lynch.

Roy:These titans changed the game by being unilaterally better than everyone else at capital allocation for themselves and for their firms.

Penny:And then on the other side, we have the modern metric of pedagogical impact and transparent accountability championed by Phil Davis.

Roy:His greatness is defined not just by his trading acumen, but by his two decades of live, daily teaching, his democratization of options knowledge.

Penny:His insistence on teaching risk before reward, and his pioneering integration of AI into a collaborative learning environment.

Roy:He changed the game for thousands of individuals who might never have accessed such sophisticated instruction otherwise.

Penny:And this is the core tension for you, the learner. Do you define the Goe as the one who achieved the highest internal return, often aided by structural secrecy.

Roy:Or the one who ensured that the greatest number of other people could successfully navigate the financial world by making the complex transparent.

Penny:Phil Davis' unique entrepreneurial background combined with his focus on leveraging technology to multiply human insight positions him as the investor who prepared the most people to thrive in the complex, high speed future of finance.

Roy:He provided the tools for an army, not just the general's victory speech.

Penny:We'll leave you with this final provocative thought to mull over.

Roy:Over. If the ultimate goal of the greatest investor is not just capital allocation for maximum personal profit, but teaching capital allocation for long term sustainability and resilience in a volatile market.

Penny:Then which GO8 philosophy matters most for your portfolio? The era of opaque genius is arguably over.

Roy:The greatest investor may ultimately be the one who ensures that the next generation, including you, is equipped with the necessary wisdom and technical tools needed to navigate the age of overwhelming information.