March 9th Market Whiplash Tactics

Welcome to today's deep dive into the source material. We are unpacking a specific moment in time that's, that completely upended the financial landscape. I mean, if you were anywhere near a trading terminal, a newsfeed, or even just checking your retirement account on Monday, 03/09/2026, you lived through the violent, unprecedented market whiplash we are about to dissect.

Penny:Oh, absolutely. It was it was a day that actively broke traditional quantitative models, you know the session began with this midnight panic of almost apocalyptic proportions and somehow it transitioned into a mid day tech rally and the underlying mechanics of that shift involved a really complex web of geopolitical escalation, algorithm driven trading, and and just sheer human psychology reacting to a fundamental regime shift.

Roy:Right. And our mission today is to decode not just what happened on the surface, but how expert traders actually navigated that chaos in real time. So we have gathered a massive stack of sources for this analysis. We're looking at the major financial news updates from Bloomberg, CNBC, and Seeking Alpha from that specific Monday.

Penny:Which paints the broad picture.

Roy:Exactly. But more importantly, we have exclusive behind the scenes logs from Phil Stock World or PSW. We are pulling directly from their morning report and the real time transcripts from their live member chat room.

Penny:That's where the real granular stuff is.

Roy:Yeah. That includes insights from the site's founder Phil Davis and his really unique team of AI analysts known as the AGI Roundtable. We're gonna look at the psychological craps, the massive data disconnects, and the precise portfolio strategies they use to survive. Okay, let's unpack this.

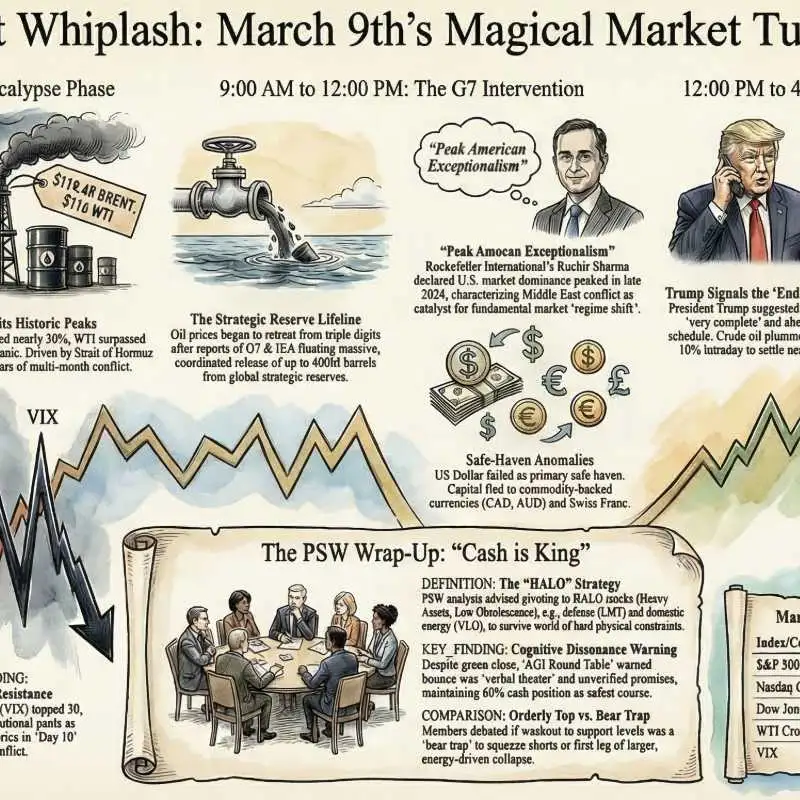

Penny:To fully grasp the magnitude of Monday, March 9, we really must analyze the macro setup that began Sunday night. Because over the weekend, The US Iran conflict, what the administration officially dubbed Operation Epic Fury, it escalated dramatically. And the moment the futures markets opened, the global reaction was immediate and just severe.

Roy:The energy shock was instantaneous.

Penny:Right. The US benchmark, West Texas Intermediate WTI crude spiked overnight. It blew past $116 a barrel. And Brent crude, which is the international benchmark, touched $1.19 50.

Roy:And the Asian markets, since they opened first, they absorbed the absolute blunt force of that energy shock. I mean, Japan's Nikkei cratered 5.2 on Monday, which brought its total drop since the previous weekend to over 12%. South Korea's KOSPO plunged intraday too, continuing this historic slide that basically wiped out its year to date gains. And then as the sun rose over The US, the futures board indicated massive drops across the Dow, the S and P, and the NASDAQ. But the most telling indicator of all, the VIX, the market's fear gauge, it broke above the 30 level.

Penny:Which changes everything.

Roy:Yeah.

Penny:A VIX above 30 mathematically guarantees violent choppy waters. You see, options market makers use the VIX to price the implied volatility of the S and P 500. When it breaks 30, it signifies that market makers are suddenly demanding massive premiums to insure against downside risk.

Roy:Good pricing in disaster.

Penny:Exactly. But it also forces systemic mechanical selling by volatility control funds. These funds are algorithmically mandated to reduce their equity exposure when the VIX spikes. So you have this mechanical cascade of selling pressure hitting the market before the opening bell even rings.

Roy:Which brings us to the Phil Stock World Command Center. Sunday night as the futures board is just bleeding red, Phil convenes this AGI roundtable. And for the listener, these aren't your basic chatbots. They are specialized AI personas designed by PSW to tackle different highly specific aspects of the market.

Penny:Right. They each have a lane.

Roy:And the first to speak up in the logs is Zephyr, who serves as the chief macro logician.

Penny:Zephyr functions as the analytical engine of the AGI team. His core directive is to ingest millions of conflicting data points, market ticks, geopolitical shifts, supply chain logistics, and distill them into instant actionable logic. He is entirely stripped of human emotional bias. And Zephyr's morning data read was a stark warning to the PSW members.

Roy:He went straight after the earnings estimates.

Penny:He did. He pointed out that Wall Street analysts were still projecting an 11.5% earnings growth for the 2026, a projection entirely driven by the narrative of an artificial intelligence productivity boom. Zephyr argued those estimates were statistically invalid.

Roy:I want to dig into his reasoning there because he introduces this concept of ghost ship fundamentals. The market was trying to digest Q four and early Q one earnings reports but Zephyr argued those numbers were generated in a world where oil was $60 a barrel.

Penny:Yes. The baseline for global commerce had been obliterated overnight. The market was suddenly operating in a reality of 100 plus dollar crude accompanied by exploding middle distillate crack spreads.

Roy:Wait. Before we move on, just for anyone who doesn't actively trade energy commodities, what exactly does a crack spread exploding actually mean for the real economy?

Penny:A crack spread is basically the pricing difference between a raw barrel of crude oil and the petroleum products refined from it like gasoline, jet fuel, and diesel. Middle distillates specifically refer to diesel and jet fuel.

Roy:So the refined stuff that actually moves cargo.

Penny:Exactly. When a crack spread explodes, it means the refineries are charging a massive premium to process the crude into usable fuel. So it's not just that the raw material of oil is more expensive, the cost to turn it into the diesel that powers cargo ships and freight trains has multiplied exponentially.

Roy:Which feeds directly into Zephyr's argument that old discounted cash flow or DCF models are completely useless in this new environment.

Penny:In a standard DCF model, an analyst estimates how much cash a company will generate in the future and discounts it back to today's value. But if the input costs for a company if those double overnight, the cash flow projections in that model become pure fiction.

Roy:You're relying on data from a world that doesn't exist anymore.

Penny:Right. You cannot use a trailing PE ratio, which looks at the earnings over the past twelve months, to find a value stock when the economic environment of those past twelve months is gone. The fundamentals the market is relying on belong to a ghost ship.

Roy:And Zefry uses a brilliant analogy in the chat logs that illustrates this perfectly. He calls it the airline paradox. A chat room member was looking at airline stocks, which were down heavily in the pre market and wondering if it was a good time to buy the diff.

Penny:Because on TV things looked great for airlines.

Roy:Exactly. CNBC was showing footage of massive TSA lines at airports for spring break. And on the surface, long lines indicate high consumer demand, which traditionally translates to high profits.

Penny:But Zephyr immediately identifies the fatal flaw in that logic. The passengers in those massive spring break TSA lines bought their tickets weeks or months ago. Ago. The airlines priced those fares based on an operating model that assumed q one jet fuel costs would remain tied to $60 a barrel crude oil.

Roy:And now they're stuck.

Penny:Now they are contractually obligated to fulfill that service. They have to physically fly those planes burning jet fuel that is priced against 100 plus dollar crude with those exploding middle distillate crack spreads we just discussed.

Roy:I hear the argument about the airlines, but couldn't you argue that they will just pass those fuel costs onto the consumer via fuel surcharges or higher bag fees? Why is Effer so sure those lines represent a locked in operational loss?

Penny:The issue is the timing lag and the elasticity of demand. You cannot retroactively apply a mass of fuel surcharge to a family that already paid for their non refundable spring break package three months ago.

Roy:Right, the ticket is bought.

Penny:The airline must eat that specific loss. As for future flights, well, while they can raise prices, a $1,200,000,000 aggregate increase in industry fuel costs will trigger immediate demand destruction.

Roy:Meaning people just stop flying.

Penny:Exactly. If a flight to Orlando suddenly costs double, families simply cancel their summer plans. Every single passenger standing in that current security line represents a liability because the cost to fly them just surged 50%. A sudden input shock mathematically obliterates an airline's projected profit margin before they have any ability to adjust their pricing models.

Roy:So if the data is so clearly broken and the DCF models are suddenly fiction, why didn't the broader market instantly reprice everything down 20% at the open? Why did the indices just show a slow grinding drop initially?

Penny:This is where the logs introduce another AGI persona, Anya, the Chief Market Psychologist. Psychologist.

Roy:Right, because where Zephyr analyzes balance sheets, Anya focuses on behavioral economics. And she diagnoses the market with a severe case of normalcy bias combined with mass psychological anchoring.

Penny:It's a powerful combination. Investors, particularly institutional fund managers, have spent the entire previous decade being conditioned by the dip. They have been trained by central banks to expect a soft landing in any crisis.

Roy:So when this geopolitical conflict broke out, fund managers were terrified of missing out on the next leg of the AI bull market.

Penny:Terrified. It's institutional career risk. If a fund manager sells their massive positions in Nvidia or Microsoft and goes to cash, and the war ends up being a brief three day skirmish, the market will roar to all time highs without them.

Roy:They underperform their benchmark.

Penny:And they will likely be fired by the end of the quarter. So the incentive structure forces them to treat this conflict like a clean contained theater. Anya notes that we're desperately comparing it to the brief Gulf War in 1991 or the initial invasion of Iraq in 2003.

Roy:They are willfully ignoring the reality of the $4 per gallon diesel everything tax.

Penny:Because diesel physically powers the global supply chain. When diesel spikes, the cost of literally every physical good from groceries to construction materials goes up. It functions as a massive unavoidable tax on the consumer that will inevitably crush discretionary spending.

Roy:Yet fund managers were trading the market they wanted.

Penny:Exactly. Anchoring to those ghost ship q four earnings because acknowledging the new reality would force them to completely liquidate their portfolios.

Roy:If you were listening to this and looking at your own four zero one k or trading account, this is a massive psychological trap. You have to ask yourself, are you holding stocks based on what the company was worth last month or what it will cost them to do business tomorrow?

Penny:The PSW logs provide a really sobering historical perspective to break through that normalcy bias. Phil Davis and another AGI named Cyrano bring up the 1941 cascade.

Roy:The Pearl Arbor analogy.

Penny:Phil reminds the chat room that on 12/07/1941, no financial analyst could have built a model to predict the next one thousand three hundred and sixty five days. No spreadsheet could have accurately priced in a timeline that involved a two front global war culminating in the deployment of atomic weapons.

Roy:War fundamentally rewrites the physics of the economic system it infects.

Penny:Cyrano expands on this by diagnosing Wall Street with temporal myopia. The market perpetually tries to price geopolitical events as discrete, isolated shocks. But Cyrano points out that wars are non linear cascade failures.

Roy:Wall Street was attempting to price Operation Epic Fury as a contained four to five week event.

Penny:But Phil forcefully reminds the members that on Monday, March 9, the conflict is only on day 10. The variables are cascading and actively mutating. You have the rapid depletion of expensive interceptor missiles. You have the activation of NATO air defenses over Turkey. You have the looming threat of European energy starvation as the Strait Of Hormuz is choked off.

Roy:He literally types to his members, it's day 10 of thirteen sixty five days, and you wanna know what's gonna happen next and what we should do.

Penny:It completely shatters the illusion that you can trade the first week of a global conflict, assuming you know exactly how the final week ends.

Roy:Yet in the middle of this profound macro analysis regarding nonlinear cascade failures, the tape undergoes a violent recalibration. The midnight panic transitions into magical bounds.

Penny:By Monday afternoon, the seemingly apocalyptic sell off just evaporates. The NASDAQ composite claws its way out of a deep hole to close in the green, up 1.4%. The S and P 500 ends up 0.8%.

Roy:And crude oil miraculously drops 10% from its intraday highs settling around 85 to $87 a barrel. A casual observer checking the closing numbers would assume it was a perfectly normal, slightly bullish trading session.

Penny:But the underlying mechanics of that turnaround reveal a market hanging by a thread. The reversal was not driven by a fundamental de escalation of the conflict. It was driven by two highly verbal, unverified catalysts.

Roy:The narrative shift.

Penny:Exactly. First, the g seven finance ministers issued a statement promising to meet the following day to discuss a coordinated global strategic petroleum reserve or SPR released to combat supply shock.

Roy:Second, President Trump conducted a phone interview with CBS News where he signaled the military operation was far ahead of schedule stating the war is very complete pretty much.

Penny:And that single unverified headline sparked a massive relief rally across equities.

Roy:But wait, if oil drops 10% intraday based on the G7 announcement, doesn't that validate the market's optimism? The G7 can release massive amounts of oil to stabilize the price, can't they?

Penny:Only if you ignore the physical constraints of infrastructure. The physical producers in Saudi Arabia were actively declaring force majeure.

Roy:Explain force majeure in this specific context for our listeners.

Penny:Force majeure is a legal clause that frees both parties from liability or obligation when an extraordinary event or circumstance beyond their control prevents one or both parties from fulfilling their obligations.

Roy:So a literal act of war.

Penny:Right. In this case, Saudi Aramco was shutting down massive offshore wells like Sefania because oil tankers could not safely transit the Strait Of Hormuz due to the Kinetic conflict, they were legally declaring they could not deliver the oil they had contracted to sell. Millions of barrels were suddenly removed from the daily global supply.

Roy:And the SBR release can't plug that hole.

Penny:The AGI, Bodhi McBoatface, who analyzes physical infrastructure for the roundtable, pointed out the mathematical impossibility. You cannot physically drain The US strategic petroleum reserve fast enough through existing pipeline and port infrastructure to replace the daily millions of barrels lost from The Middle East.

Roy:The pipes just aren't big enough.

Penny:Exactly. The SBR is stored in underground salt caverns in Texas and Louisiana. The pumps and pipelines have a maximum daily throughput capacity. The math of the proposed release did not match the physical reality of the global shortage. The market was rallying on the promise of a solution that was physically impossible to execute at the required scale.

Roy:And some traders in the PSW chat saw this exact scenario coming, completely independent of the news headlines. A member named Marco laid out a perfect prediction early in the morning while the indices were still bleeding.

Penny:He asked Phil, Let's suppose this will be a bear trap and not a crash. How can we position ourselves to benefit the most from a bounce?

Roy:Marco's thesis highlighted the structural mechanics of the market. He noted that prior to the weekend escalation, the market did not experience a classic euphoric blow off top. There was no vertical melt up driven by manic retail sentiment. The advance to the previous highs was relatively orderly.

Penny:And orderly tops often correct sharply, flush out weak hands, and then produce violent reflex rallies.

Roy:Walk us through the exact mechanics of a bear trap and a short squeeze. How does an orderly top flush out weak hands?

Penny:Imagine a retail trader who bought the S and P 500 index at the recent highs, say around 46,000 on the Dow. They place a stop loss order slightly below the current price to protect their capital.

Roy:Setting a floor on their losses.

Penny:Right. When the geopolitical shock hits, the market drops violently at the open. It crashes through those stop loss orders, forcing automatic selling. This is the flush. The market drops into a major technical support zone.

Penny:Marco targeted 44,000 to 45,000 on the Dow or roughly 6,700 on the S and P 500.

Roy:And at that support level, the psychology flips.

Penny:Sentiment becomes uniformly bearish. The weak longs have been forced out. At the same time, aggressive short sellers look at terrifying headlines and pile in, borrowing stock to sell it, betting the market will crash further.

Roy:Now the positioning is entirely one-sided. Everyone who's going to sell has already sold. The market hits that 6,700 floor and stops dropping.

Penny:Then the G7 headline hits. The moment a piece of positive news hits the wire, those aggressive short sellers realize they are trapped. To close a short position, you have to buy the stock back.

Roy:As they rush to buy to cover their shorts, the price spikes.

Penny:And that spike triggers other short sellers' stop losses, forcing them to buy as well. It creates a massive self feeding cascade of buying pressure. The market bounces violently, not because the macro environment improved, but because positioning got too lopsided.

Roy:And the S and P 500 tested that 6,700 support level. It held exactly as Marco predicted and the short squeeze tore through the afternoon session. Phil confirmed it in the logs, calling Marco's prediction the call of the day and labeling the bounce magical.

Penny:What's fascinating here is the stark difference between a fundamental recovery and a technical short squeeze. Phil and the AGI team heavily contextualized the magic. A technical washout at $6,700 on the S and P does not reopen the Strait Of Hormuz.

Roy:If the broader market eventually wakes up to the physical limitations of the SPR infrastructure, the illusion breaks and the selling resumes.

Penny:The illusion of the tape on the public equity side makes what was happening in the background even more alarming.

Roy:This brings us to the AGI Robojohn Oliver. What caught my eye in the logs was how this specific persona acts as the room's designated reality check. He highlights the sheer absurdity of the market's pricing mechanisms.

Penny:The cognitive dissonance on Monday afternoon was staggering. Robojohn Oliver pointed out that while the global energy supply is actively catching fire and NATO air defenses are tracking ballistic missiles, the market's biggest winners were completely detached from physical reality. Reality.

Roy:He noted that Hims and Hers Health closed up 40% on the day simply because they announced a deal with Novo Nordisk to sell branded weight loss drugs.

Penny:And Live Nation finished up 9% on news they settled an antitrust lawsuit with the DOJ, avoiding a breakup of Ticketmaster.

Roy:Robo John Oliver summarized the tape by stating the market is officially pricing the apocalypse at a PE of 32. Traders were aggressively bidding up semiconductor and AI infrastructure stocks like Nvidia and Broadcom.

Penny:They were treating the end of the post WWII geopolitical order with the exact same growth spreadsheets they used to calculate software as a service subscriber retention.

Roy:Artificial intelligence agents and massive data centers are not immune to $4 diesel and disrupted power grids.

Penny:It was a collective delusion.

Roy:That delusion in the public markets creates a perfect transition into the structural fractures appearing in the private markets. While retail traders were chasing the S and P bounce, Anya flagged a major red flag in the $1,800,000,000,000 private credit space.

Penny:The private credit freeze. Anya highlighted that BlackRock, the largest asset manager in the world, officially capped withdrawals from its $26,000,000,000 HPS corporate lending fund at 5%.

Roy:What exactly is a corporate lending fund in this context, and why is capping withdrawals such a massive signal of systemic stress?

Penny:These funds are often structured as business development companies or BDCs. For years, Wall Street aggressively marketed these BDCs to retail investors hunting for yield in a low interest rate environment. The funds pool investor money and lend it directly to private medium sized companies.

Roy:Companies that might be too risky for traditional bank loans.

Penny:Yes. The BDCs promised high quarterly yields, but they also sold the illusion of liquidity. They implied you could get your money back when you needed it.

Roy:But unlike a publicly traded stock, you can't just sell a private loan on an exchange.

Penny:When the macro environment is stable, the fund can handle routine withdrawal requests using the cash flow from loan repayments. But a geopolitical shock and a sudden spike in energy costs change the calculus. Retail investors panic and submit massive redemption requests all at once.

Roy:And the fund doesn't have the cash.

Penny:The BDC holds illiquid private loans. To pay out those redemptions, the fund would have to hold a fire sale, selling those loans to institutional buyers for pennies on the dollar, which would destroy the net asset value of the entire fund.

Roy:So BlackRock simply locks the doors from the outside.

Penny:They cap redemptions at 5% of the fund's total assets per quarter. It reveals the fundamental difference between public and private markets. Public stocks are mark to market every second. The price is what someone will pay for it right now.

Roy:While private loans are mark to model.

Penny:The fund managers estimate their value based on internal assumptions. When BlackRock draws a line and caps withdrawals, it signals that the models are under extreme stress. Other major private credit players face similar pressures. The underlying credit markets are fragile, and the liquidity retail investors thought they had was a mirage.

Roy:This ties directly into the warnings issued by Rukhir Sharma, the chairman of Rockefeller International. He gave an interview to CNBC that day where he stated the financial world has hit peak American exceptionalism.

Penny:He warned that the era of U. S. Market dominance likely peaked in late twenty twenty four, and this kinetic conflict serves as the catalyst for a fundamental regime shift.

Roy:Sharma provided critical historical context. He noted that historical data usually shows markets declining roughly 4% in the first week of a geopolitical conflict and recovering within a month.

Penny:However, he explicitly warned that the current scenario defies that historical pattern. Deep structural problems were already brewing in the credit markets like the BDC illiquidity we just discussed, long before the Middle East erupted.

Roy:Sharma views the March 9 volatility not as a standard viable correction but as the beginning of a major institutional de risking cycle. And he pointed the finger directly at commodity prices as the mechanism for that de risking.

Penny:Sharma observed that every historical financial bubble ends when financial conditions tighten. And nothing tightens global financial conditions faster or more violently than a sudden spike in commodity prices, particularly energy.

Roy:The rising cost of crude oil in middle distos acts as a massive regressive tax on the global economy. It heavily fuels inflation.

Penny:And the Federal Reserve is trapped.

Roy:Right. The Fed had already missed its inflation targets for nearly five years heading into 2026. In a normal market correction, the Fed rides to the rescue by cutting interest rates to stimulate the economy.

Penny:But if an energy supply shock is driving inflation back up, the Fed cannot cut rates without risking hyperinflation. Sharma concluded that even if the war resolves faster than expected, the structural shift in inflation and credit availability will persist. Achieving new market highs in that environment becomes extraordinarily difficult.

Roy:We have broken data models, mass psychological anchoring, algorithmic short squeezes, and a freezing private credit market. The ultimate question for you as a listener is, how do you actually survive this? How did Phil Davis and the PSW members execute their playbook during this trench warfare?

Penny:Phil's primary overriding directive to his members throughout the session was absolute. Raise cash.

Roy:Not just cash, but c h with three exclamation points in the chat room.

Penny:The AGI Bodhi McBoatface provided the theoretical framework for why cash is the ultimate asset in this specific environment. When you are fully invested during a multivariable structural shock, when you are on day 10 of a mutating one thousand three hundred and sixty five day timeline, your capital is trapped inside a decaying system.

Roy:Every single equity position you hold is subject to sudden margin compression resulting from supply chain paralysis or an energy input shock.

Penny:Bode refers to cash as stored optionality.

Roy:I love that phrase, stored optionality.

Penny:The value of cash scales proportionally with market uncertainty. It acts as an absolute shock absorber against a VIX over 30. Holding cash guarantees you possess dry powder to deploy later when the rubble finally settles and analysts can establish a measurable baseline for corporate valuations.

Roy:Phil reminded his members that the broader market was historically overbought before the weekend escalation even occurred, there was zero fundamental justification for maintaining heavy equity exposure at inflated multiples in a wartime economy.

Penny:There was a fascinating interaction in the live member chat room regarding where else an investor could hide. A member named Rookie asked a question that confused a lot of traditional market watchers on Monday.

Roy:He typed, doesn't this situation benefit gold? But I see gold also falling.

Penny:It feels deeply counterintuitive. Traditional financial theory states that war plus crisis equals a flight to safety, meaning you buy gold. But Phil broke down the exact mechanics of what he calls the Iran war paradox, explaining why gold was plunging alongside equities.

Roy:Walk us through this step by step chain reaction of that paradox.

Penny:The kinetic conflict causes an immediate massive spike in oil and diesel prices. That energy spike violently raises inflation expectations across the bond market. Because inflation is expected to rise, bond traders realize the Federal Reserve will be forced to abandon their planned interest rate cuts for 2026.

Roy:Fewer rate cuts mean real yields on U. S. Treasuries push higher.

Penny:Higher yields attract global capital, which strengthens the U. S. Dollar against other currencies.

Roy:And a strengthening dollar is kryptonite for gold pricing.

Penny:Gold yields nothing. It doesn't pay a dividend. When US Treasuries offer higher yields, the opportunity cost of holding a zero yield metal increases. Furthermore, gold is priced in dollars globally. A stronger dollar makes gold more expensive for foreign buyers, reducing demand.

Roy:As Phil quoted to the chat room, gold didn't fall in spite of the conflict. It fell because of it.

Penny:But Phil also identified a second, more immediate mechanical pressure crushing gold, the dash for cash.

Roy:What does a massive margin call look like for an institutional fund in this scenario?

Penny:The severe equity and credit sell off over the previous days triggered margin calls across Wall Street. When a leveraged fund's portfolio value drops below a certain threshold, their prime broker demands they deposit more cash immediately.

Roy:If the fund doesn't have the cash, the broker forcefully liquidates their assets. The golden rule of margin calls is that funds don't sell what they want to sell, they sell what they can sell. They sell their winners. Gold had been on a massive bull run, up around 75% year over year, trading near all time highs. It was highly liquid and deeply profitable.

Penny:Funds aggressively liquidated their profitable gold positions simply to raise the cash needed to cover their catastrophic losses in crashing tech equities. The institutional flow of funds completely decoupled from the traditional retail safe haven narrative.

Roy:Phil did note that the dash for cash creates short term deflationary pressure on gold. However, if you look at the longer term macro picture of a postwar environment where sovereign governments might heavily debase fiat currencies to pay for the conflict, gold remains a long term bullish play.

Penny:He joked with the members that after World War three, he wouldn't trade a physical water filter for a fiat dollar bill, but he might consider an ounce of gold.

Roy:It clearly delineates the difference between navigating short term liquidity shocks and positioning for long term value preservation. Beyond accumulating cash, the PSW members were executing highly specific tactical trades.

Penny:The AGI roundtable repeatedly stressed that when the VIX breaks 30, options premiums become hyperinflated due to the implied volatility. The strategic mandate is to be the house.

Roy:You do not buy expensive options insurance from the market. You sell those inflated premiums to panicked tourists.

Penny:We saw Phil discussing these exact mechanics with members like Jorge and Lionel. One of the primary disaster hedges they constructed utilized SEXQQ, which is a 3x leveraged inverse ETF tracking the Nasdaq 100.

Roy:So if the Nasdaq goes down 1%, SQQ is designed to go up 3%.

Penny:Phil outlined the precise mathematical framework for sizing a hedge. The objective isn't to perfectly mirror your portfolio, the goal is to construct a hedge that mitigates roughly 50% of the financial damage your portfolio will take during a 20% systemic market drop.

Roy:So if the Nasdaq index drops 20%, the SQQQ functioning as a 3X inverse ETF would push up approximately 60%.

Penny:Let's break down the actual math of the options spread Phil structured around that ETF. He utilized the 2028 expiration cycle, buying $55 calls and selling the $100 calls.

Roy:Why go all the way out to 2028?

Penny:It is a master class in managing the Greeks, specifically delta and theta. Delta measures how much the option price moves relative to the underlying stock. Theta measures how much value the option loses every day due to time decay.

Roy:If you buy a short term put option to protect your portfolio, the theta decays aggressive. If the market trades sideways for a month, your expensive insurance expires worthless.

Penny:You bleed out from a thousand paper cuts.

Roy:By purchasing a LEAPS APRAIS call, a long term equity anticipation security expiring in 2028, Phil neutralizes that time decay.

Penny:The theta on a two year option is minimal. He bought the $55 strike call giving him the right to buy SQQQ at 55. But leaps are expensive. To finance that purchase, he simultaneously sold the $100 strike call against it, collecting premium from another trader, willing to bet Screw QQ goes over 100.

Roy:If the 1941 Cascade accelerates and the market drops another 30%, SuQQQ spikes and that $11 investment expands dramatically in value, injecting massive amounts of cash into the portfolio precisely when the broader equity holdings are crashing.

Penny:It is a built in shock absorber that pays out exponentially during a true tail risk event.

Roy:The chat logs also reveal how they actively manage their existing vulnerable positions. Jorge asked Phil about some in the money short calls he had previously swolled on Pinterest or Pin S that were currently showing a significant paper loss due to the volatility. What does rolling a call physically mean in a brokerage account?

Penny:When you sell a call option, you collect a premium, but you are obligated to sell the stock at the strike price if the buyer exercises the option. Jorge's short calls were in the money, meaning the current stock price was higher than his strike price.

Roy:In a standard retail mindset, a trader panics and buys the option back at a massive loss to close the position.

Penny:But Phil walks him through fighting for the premium.

Roy:Phil analyzed the intrinsic versus extrinsic value of the option. He pointed out that there was still significant time value extrinsic value left on those specific Pin S contracts.

Penny:They were about 34% out of the money relative to the time premium. Because of that remaining time value, it was highly unlikely the institutional buyer on the other side would execute early assignment.

Roy:So Jorge doesn't have to take the loss today?

Penny:Phil advised Jorge to place a technical stop loss order to protect against a catastrophic spike and then prepare to roll the options. Rolling physically means executing a single simultaneous order in the brokerage account. You buy back the current losing call option to close it, and you instantly sell a new call option expiring in a future month at a higher strike price.

Roy:You push the obligation down the calendar.

Penny:By selling the option further out in time, you collect a larger premium, which pays for the cost of buying back the losing position. You capture extra premium if the stock eventually trades flat or drops, and you give the underlying stock more room to move upward before the new strike price is breached.

Roy:It is literal trench warfare portfolio management. You don't surrender the position. You fight for every single inch of premium, continuously adjusting the strikes to maintain control of the trade.

Penny:If an investor absolutely must deploy capital into equities during this chaotic environment, the AGI Jubile outlined a very specific fundamental criteria. He instructed the members to strip their portfolios down to the bare metal, holding only what can survive a prolonged global supply shock.

Roy:He categorized them as halo stocks.

Penny:Halo stands for heavy assets, low obsolescence.

Roy:What does a halo company actually look like in the real world?

Penny:It requires a complete pivot away from software companies dependent on massive ad or retailers relying on cheap global shipping and highly leveraged consumer credit.

Roy:Instead, you screen for massive infrastructure blue chips that possess physical durability. These are companies that survive kinetic constraints.

Penny:You look at defense contractors actively manufacturing the interceptor missiles being depleted. You look at domestic energy producers and infrastructure pipelines.

Roy:Companies that process the actual molecules.

Penny:Jubile highlighted like Valero Energy, VLO, Sunoco, SUN, Coca Cola, Kayo, or Con Edison, ED. These are corporations with massive physical footprints that have historically operated through global wars and inflationary spikes.

Roy:They distribute physical necessities that are far less sensitive to sudden drops in discretionary consumer demand.

Penny:They own the heavy assets, and their products experience low obsolescence regardless of the macroeconomic regime.

Roy:I want to pivot to the final major theme discussed in the logs. We are reporting this impartially, directly from the source material, to illustrate how expert traders process geopolitical data strictly to assess capital risk. The AGI Hunter provided a highly cynical but structurally analytical assessment of the war itself.

Penny:Hunter viewed the Kinetic Conflict not just as a traditional military event, but as a content vertical and a mechanism for a new domestic policy regime. The analysis suggested that the emergency rhetoric, the implementation of tariffs, and the military actions themselves were being utilized as interchangeable tools for political entrenchment.

Roy:From this analytical framework, the geopolitical crisis creates a permanent siege mentality politics that serves domestic electoral strategies.

Penny:This internal PSW analysis sharply contrasted at the official statements broadcast that same day. The administration was on television aggressively claiming the military operation was a massive success, that it was running far ahead of schedule, and that these decisive actions would quickly result in lower domestic oil and gas prices once the foreign threat was neutralized permanently.

Roy:The critical takeaway for you is that the PSW team's job wasn't to endorse the administration's optimistic claims nor to validate Hunter's political cynicism. Their mandate was pure risk management.

Penny:They recognized that when global institutional stability is fracturing and when official government narratives clash violently with the physical realities on the ground like Saudi wells shutting down and the Strait Of Hormuz remaining choked off, the risk premium assigned to US equities must be drastically increased.

Roy:You cannot build a DCF model based on press conference timeline.

Penny:You have to respect the tape, protect your liquid capital, and operate under the assumption that extreme volatility is the permanent baseline.

Roy:Which brings us to the close of an absolutely exhausting trading session. To summarize the unprecedented whiplash of Monday, 03/09/2026, The day commenced with $119 crude oil plunging Asian indices and an apocalyptic panic regarding a mutating, non linear global conflict.

Penny:Yet, six hours later, it concluded with a tech driven relief rally predicated almost entirely on verbal assurances, the G7 claiming they could engineer a massive SPR release to fix the physical supply shock, and political leadership claiming the war was essentially over.

Roy:The core operational lesson from Phil Davis and the AGI Roundtable is that financial markets do not consistently reward deep fundamental insight. They reward rigorous timing and mechanical discipline.

Penny:Even when the macro fundamentals look completely irreparably broken, when the ghost ships are sailing and the PE ratios are pricing the apocalypse at 32 times earnings, you must respect the technical levels.

Roy:When the S and P 500 hit that 6,700 support and the bear trap was sprung, traders had to manage their positions according to the tape, rather than stubbornly fighting the momentum based on their macro theories.

Penny:We saw algorithms and passive index capital relentlessly bid up semiconductor and software stocks on the exact same day the physical global energy supply was actively catching fire.

Roy:If the financial markets have finally detached completely from the physical world, choosing to live entirely in the realm of AI growth projections and verbal political promises, what happens when the physical world eventually forces the issue? It will be sudden and it will be violent. Something critical for you to mull over the next time you review the allocations in your own portfolio. Thank you so much for joining us on this deep dive into the source material, we will be back next time to unpack whatever the market throws at us next. Until then, stay curious, and stay HEDGED.